{kind=link}

Strong African economies can be created on the back of efficient transport solutions and investments.

Well-functioning transport networks are the heartbeat for many nations, bringing with them several social and economic opportunities at city, regional, and country levels. For Africa, last-mile delivery is a growing opportunity storm transport sector. What gave rise to the storm, who will ride or sink and where are the highest areas with potential? African cities are seeing extraordinary growth, with over 60 percent of Africans expected to live in cities by 2030. With this comes higher demands for efficient supply chains for growing urban areas and the remaining rural space to avoid expansion of the rural-urban divide. The year 2020 highlighted the extent of this crack in many local supply chains, but also accelerated the growing e-commerce in Africa. Now, two years down the line, there are lessons learned and several opportunities tapped, evident by the rise in transport start-ups. In 2021 alone, 21 transport start-ups were established in Africa, addressing digitisation, last-mile delivery solutions, increasing safety, etc.

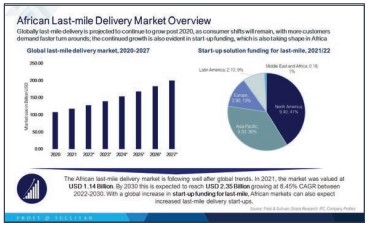

The African last-mile delivery market was valued at US$1.14 billion in 2021. By 2030, this is expected to reach US$2.35 billion. The industry can be segmented into categories by product, industry, sales channel, delivery type, service speed, and geography. Based on current trends, players with the fastest turnaround times across all categories will enjoy the largest growth. The waiting time for consumers has been cut from the previous five to six days to one-day or same-day delivery services. The shift has created ripple opportunities for establishing efficient sales channels.

Digital communication platforms that allow for easy returns, exchanges, and increased connectedness between client and vendor are also gaining ground. Aside from newer entrants, even larger industry giants are also creating innovative models to reduce shipping costs and ride this opportunity wave. Region expansions of both newer entrants and established players are in Egypt, South Africa, Nigeria, Ivory Coast, Tunisia, Ghana, Ethiopia, Zambia, Kenya, and other markets. With most of the regions, the growth needs to be met by additional investments in key infrastructure (physical and digital) to ensure long-term solutions.

Overall, the high-potential areas by segments in the next decade are expected to be through growth in B2C models (by product type), e-commerce (industry), the distributor segment (by sales channel), and parcel services (by delivery type). In South Africa alone, the projected revenue generated by e-commerce is US$7.07 billion for 2022, with an expansion to US$14.90 billion by 2027 (at a CAGR of 16.09 percent from 2022-2027). User penetration is expected to rise from 45.1 percent in 2022 to 58.1 percent by 2027. This trend is compared to changes in the global market, but Africa has the potential to leapfrog failures from its predecessors. With the growth in global funding for last-mile delivery solutions, Africa is not without examples to learn from. This beautiful storm could, however, be cut short if challenges in supporting infrastructure and restraints like corruption (delivery sector) are not addressed.

Africa is open and hungry for business and has taken strides in showing this. With key frameworks like the African Continental Free Trade Area (AfCFTA) in place (targeting to increase intra-trade), efficient delivery solutions are here to stay and last-mile delivery is one of those.